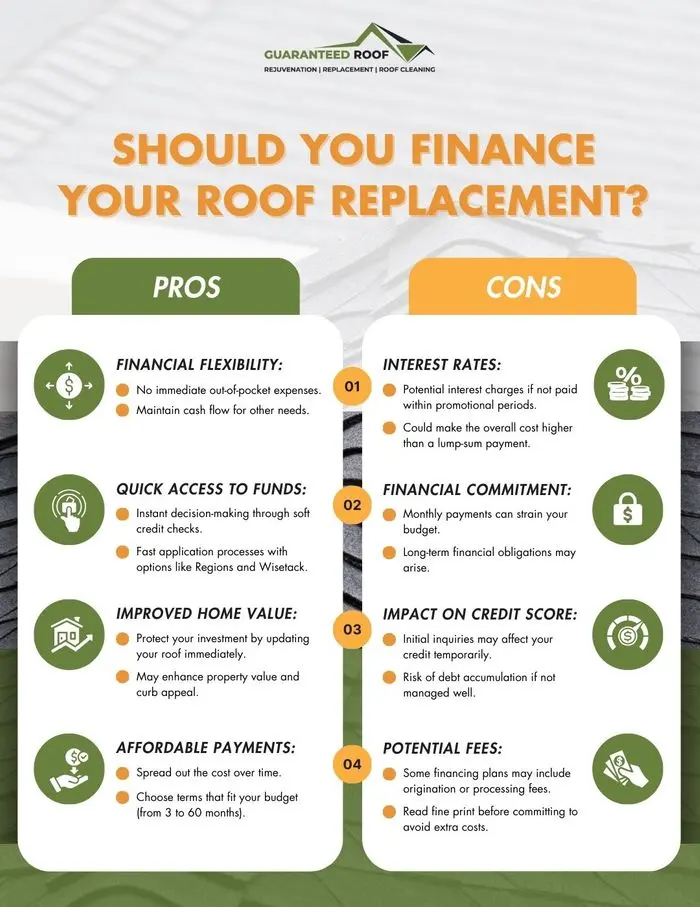

Homeowners looking to replace a deteriorating roof often wonder how to fund the project without draining savings or incurring unmanageable debt; the most effective solution is to compare the range of specialized roofing financing options, weigh interest rates, repayment terms, and eligibility requirements, and then choose the plan that aligns with both budget constraints and long‑term home‑value goals. Understanding the nuances of each financing avenue—whether a home equity line of credit, a low‑interest loan from a credit union, or a government‑backed grant—can turn a costly emergency into a strategically financed investment.

Why Traditional Savings Often Fall Short

Even for households with a solid emergency fund, a full roof replacement can easily exceed $10,000, especially in high‑cost markets such as California. According to the Roofing Contractor Association’s 2026 market report, the national average for a 2,000‑sq‑ft roof sits between $8,500 and $12,300, with premium materials pushing the total above $15,000. Relying solely on cash reserves not only depletes liquidity but also eliminates the opportunity to benefit from low‑interest financing that can preserve cash flow for other home‑improvement projects.

Top Financing Vehicles for Roof Replacement

1. Home Equity Line of Credit (HELOC)

A HELOC leverages the equity built into your property, offering a revolving credit line that typically features variable rates ranging from 4.5% to 7.5% APR in 2026, according to the Federal Reserve’s Consumer Credit Survey. The flexibility to draw only the amount needed for the roofing contract makes it a popular choice for homeowners who anticipate future upgrades, such as adding solar panels or upgrading insulation.

Table of Contents

- Why Traditional Savings Often Fall Short

- Top Financing Vehicles for Roof Replacement

- 1. Home Equity Line of Credit (HELOC)

- 2. Home Improvement Loan (Personal Loan)

- 3. Mortgage Refinancing

- 4. FHA Title I Home Improvement Loan

- 5. Solar Roof Financing with Integrated Roofing

- Choosing the Right Option for Your Situation

- Regional Cost Variations and Their Impact on Financing

- Step‑by‑Step Guide to Secure Roofing Financing

- Step 1: Evaluate Your Financial Profile

- Step 2: Get Multiple Quotes from Licensed Roofing Contractors

- Step 3: Compare Financing Offers

- Step 4: Apply for Your Chosen Product

- Step 5: Close the Loan and Coordinate with the Contractor

- Common Pitfalls and How to Avoid Them

- Real‑World Case Studies

- Case 1: Suburban Homeowner in Florida

- Case 2: Rural Texas Property Owner

- FAQ – What Homeowners Frequently Ask

- Can I combine a HELOC with a personal loan?

- Do roofing loans affect my credit score?

- Are there any tax credits for roof replacement?

- What happens if I sell my house before the loan is paid off?

- Future Outlook: Financing Trends Through 2027

- Final Thoughts

- Pros: Interest may be tax‑deductible, high borrowing limits (often up to 85% of home value), and only pay interest on the amount drawn.

- Cons: Variable rates can increase over time; the home is collateral, so default could jeopardize ownership.

2. Home Improvement Loan (Personal Loan)

Many banks and credit unions now offer dedicated home‑improvement loans with fixed rates between 5.2% and 8.3% APR. These loans typically have terms of 3 to 7 years, providing predictable monthly payments. According to the Consumer Financial Protection Bureau (CFPB) 2026 data, fixed‑rate personal loans saw a 12% increase in approval rates for roofing projects compared with the previous year.

- Pros: No collateral required, fixed interest, quick disbursement.

- Cons: Lower borrowing limits (often $20,000 max), potentially higher rates for borrowers with lower credit scores.

3. Mortgage Refinancing

Refinancing an existing mortgage to pull out cash for a roof replacement can lock in a low, fixed rate—averaging 5.9% in 2026 per the Mortgage Bankers Association. This option is especially advantageous when current mortgage rates are lower than the original loan, allowing homeowners to reduce overall interest costs while financing the roof.

- Pros: Lower rates than most unsecured loans, potential to extend repayment term and lower monthly outlay.

- Cons: Closing costs (typically 2%–5% of the loan amount), resetting the amortization schedule may increase total interest paid.

4. FHA Title I Home Improvement Loan

The Federal Housing Administration (FHA) offers Title I loans up to $25,000 for home repairs, including roof replacement. As of 2026, the program provides fixed rates around 6.1% APR and can be combined with other financing options for larger projects.

- Pros: Accessible to borrowers with credit scores as low as 620, government backing reduces lender risk.

- Cons: Strict documentation requirements, limited to primary residence.

5. Solar Roof Financing with Integrated Roofing

When homeowners plan to install solar shingles or photovoltaic panels, many solar providers bundle roof replacement with solar financing. The Solar Energy Industries Association (SEIA) reports that bundled loans often carry rates as low as 3.8% APR, because the combined system qualifies for both energy‑efficiency incentives and roofing warranties.

- Pros: Lower overall cost due to tax credits, long‑term energy savings, and coordinated project management.

- Cons: Higher upfront costs if solar hardware is included; eligibility depends on roof orientation and structural suitability.

Choosing the Right Option for Your Situation

Selecting a financing path should begin with a comprehensive assessment of your home’s equity, credit health, and long‑term financial objectives. Below is a decision‑making framework that professionals use to match homeowners with the optimal solution.

| Scenario | Best Financing Choice | Key Reason |

|---|---|---|

| High equity, good credit | HELOC | Low rates, flexible draw schedule |

| Limited equity, need quick cash | Personal loan | No collateral, fast approval |

| Current mortgage rate > 5% and credit score > 700 | Mortgage refinance | Lock in lower rate, combine with other debt |

| Credit score 620‑680, primary residence | FHA Title I | Government‑backed, lower credit threshold |

| Planning solar installation | Solar roof financing | Bundled incentives and low rates |

Regional Cost Variations and Their Impact on Financing

Geography heavily influences both the total cost of a roof and the financing terms offered. For instance, homeowners in California face higher material and labor expenses due to stricter building codes; a recent analysis from Why California Roof Costs Differ From Other States shows an average premium of 18% compared with national averages. Conversely, Texas homeowners typically encounter lower labor rates, as detailed in the Average Roofing Replacement Cost for a 2,000‑Sq Ft House in Texas – 2026 Guide & Budget Tips. Understanding these regional differences helps you negotiate better loan amounts and anticipate the total interest burden over the loan term.

Step‑by‑Step Guide to Secure Roofing Financing

Step 1: Evaluate Your Financial Profile

Gather recent pay stubs, tax returns, and a credit report. Use free tools such as AnnualCreditReport.com to verify your score. A score above 720 typically unlocks the most favorable HELOC or refinance rates.

Step 2: Get Multiple Quotes from Licensed Roofing Contractors

Secure at least three detailed estimates that break down materials, labor, and warranties. This documentation is essential for loan applications and can be used to negotiate better terms.

Step 3: Compare Financing Offers

Create a simple spreadsheet that captures APR, total interest, fees, and monthly payment for each option. Include potential tax deductions for interest on HELOCs or home‑improvement loans, as highlighted by the IRS Publication 936 (2026 edition).

Step 4: Apply for Your Chosen Product

Submit the required paperwork—proof of home ownership, contractor estimate, and personal financial documents—to the lender. For government programs like FHA Title I, you’ll also need to complete the HUD‑approved “Application for Home Improvement Loan.”

Step 5: Close the Loan and Coordinate with the Contractor

Once approved, arrange for the lender to disburse funds directly to the roofing company. Many lenders require a lien be placed on the property, ensuring the contractor receives payment upon completion.

Common Pitfalls and How to Avoid Them

- Over‑borrowing: Requesting a loan larger than the actual roof cost can inflate interest expenses. Stick to the contractor’s final invoice.

- Ignoring variable‑rate risk: With HELOCs, a sudden increase in the prime rate can raise monthly payments dramatically. Consider a rate‑lock or a hybrid HELOC with a fixed‑rate option.

- Failing to verify contractor licensing: Inadequate workmanship can void warranties, leading to additional repair costs that your financing won’t cover. Verify licensing through your state’s contractor board.

- Neglecting tax implications: While interest on a HELOC used for home improvement is often deductible, the Tax Cuts and Jobs Act of 2022 changed the cap to $750,000 of total mortgage debt. Consult a CPA to maximize deductions.

Real‑World Case Studies

Case 1: Suburban Homeowner in Florida

Maria, a 42‑year‑old teacher in Orlando, received a $13,200 estimate for a full shingle roof replacement. By tapping into a 2026 Roof Replacement Cost Estimate for Homeowners in Florida – 2026 Guide & Budget Tips, she identified a low‑interest HELOC offering 5.2% APR. The HELOC allowed her to pay the contractor immediately while only incurring $1,080 in interest over three years, preserving her emergency fund for other family needs.

Case 2: Rural Texas Property Owner

John, a retired veteran in Lubbock, qualified for a USDA Rural Development loan that covered 100% of his $9,600 roof replacement. The loan’s 4.3% fixed rate and zero‑down structure eliminated the need for a down‑payment, illustrating how government‑backed programs can serve homeowners in lower‑income, high‑need areas.

FAQ – What Homeowners Frequently Ask

Can I combine a HELOC with a personal loan?

Yes, some homeowners use a HELOC for the primary expense and a personal loan to cover ancillary costs such as roof ventilation upgrades. However, each loan will carry its own interest rate and repayment schedule, so careful cash‑flow analysis is essential.

Do roofing loans affect my credit score?

Hard inquiries from loan applications may temporarily dip your score by 5–10 points. Consistently on‑time payments, however, can improve your credit over the loan’s life.

Are there any tax credits for roof replacement?

While the federal government does not offer a direct credit for roof replacement, energy‑efficient upgrades (e.g., cool roofs or solar integration) may qualify for the Residential Energy Efficient Property Credit, which can offset up to 30% of qualifying costs.

What happens if I sell my house before the loan is paid off?

For secured loans like HELOCs and refinances, the lien stays attached to the property. The new buyer assumes the loan or the seller must pay off the balance at closing. It’s crucial to disclose any outstanding liens to avoid legal complications.

Future Outlook: Financing Trends Through 2027

Industry analysts predict a rise in “green‑roof” financing as climate‑resilient building codes become mandatory in coastal states. According to a 2026 report by the National Association of Home Builders (NAHB), lenders are expected to bundle roof replacement with energy‑efficiency incentives, offering blended APRs below 4% for qualifying projects. Homeowners who anticipate these trends should consider financing options that allow for future upgrades, such as modular HELOCs that can be increased as additional sustainability measures are added.

Final Thoughts

Securing the best roofing replacement financing requires a disciplined approach: assess equity, compare loan structures, factor in regional cost differentials, and align the financing timeline with your home‑ownership goals. By leveraging the right mix of HELOCs, personal loans, refinancing, or government‑backed programs, you can protect your property, enhance its market value, and maintain financial stability throughout the repayment period.